Other monetized indicator systems

Other monetized indicator systems for LCA are:

– the system of CE Delft which is damage based (in fact it started as a new calculation set of the ExterneE project); the advantage of damage based systems is that they appeal to the awareness of the issue, however, the disadvantage is that the calculation is highly uncertain (inaccuracies of a factor 3 – 10 are common).

– the EPS systems which is based on the Willingness to Pay in Sweden to resolve the effects of pollution.

– the Stepwise system, which is a so called budgetary system: the part of the GNP that we can spend reasonably well on specific environmental issues, in Denmark.

– Marginal Abatement Costs, which are not applied in LCA, but in governmental policies.

Although these other indicator systems differ from philosophies, they have a lot in common in practice.

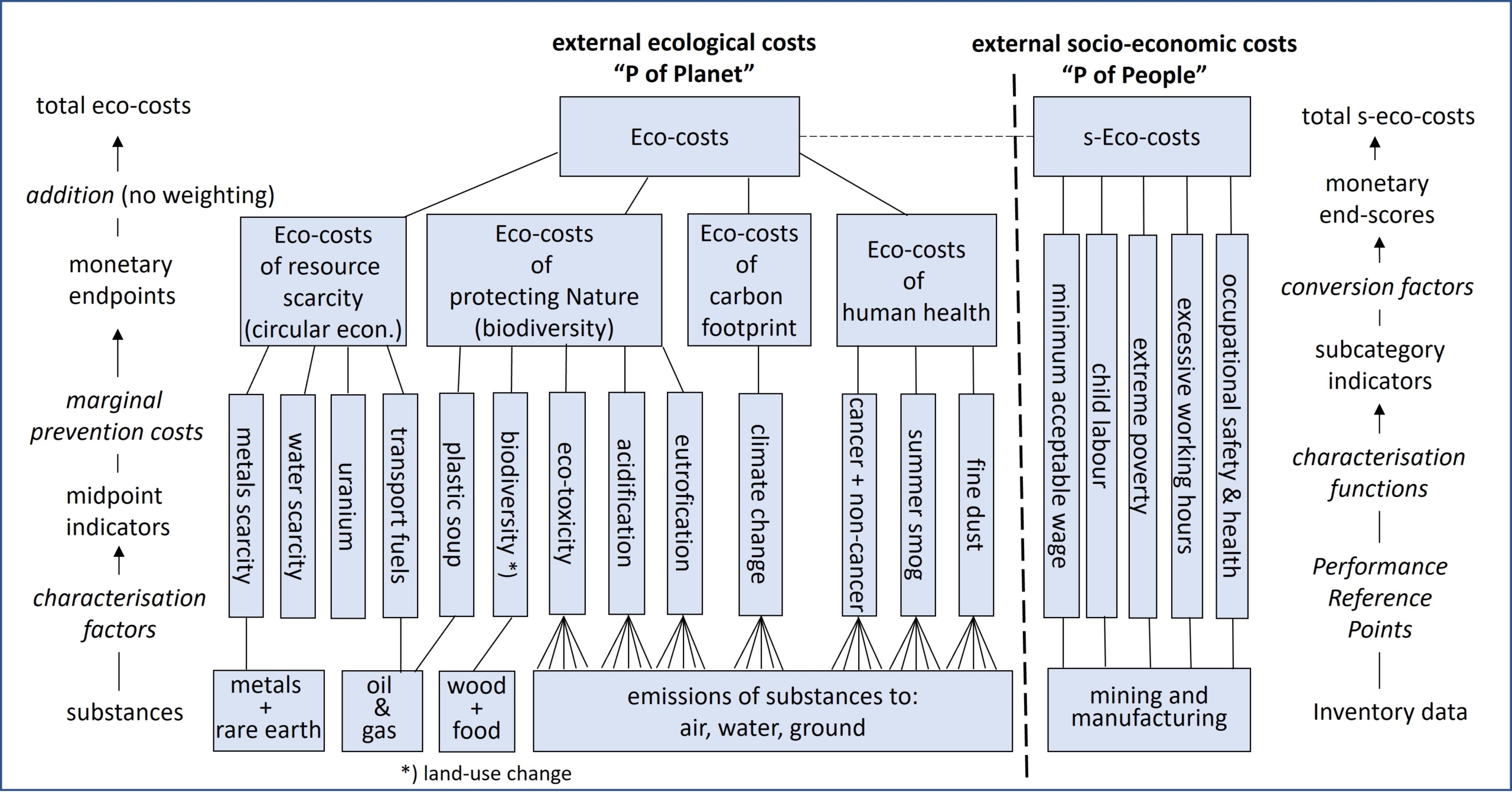

At this moment, the eco-costs is the most applied system in science. (based on the number of peer reviewed scientific papers).

The choice of midpoints, endpoints and single score indicators

ISO 14044 Section 4.4.2.2.1 has a statement that “The selection of impact categories, category indicators and chacterisation models shall be both justified and consistent with the goal and the scope of the LCA”. That means that the total eco-costs might not always the right choice in every LCA study (that is the reason that the Idemat tables provide columns for midpoints scores, not only for eco-costs but also for ReCiPe and Environmental Footprint).

It is common sense that, when a greenhouse study is done for a government, that CO2 equivalent is chosen as indicator. The same applies for NOx equivalent for a study on eutrofication of protected areas of nature. In such “one-issue” LCAs it is clear which corresponding indicator has to be selected in the first (‘goal and scope’) stage of the study, prior to the actual calculations.

In general, the classical argument is that midpoints are less inaccurate than endpoints. But there is a disadvantage of taking midpoints instead of endpoints or single score systems, as midpoint score systems in LCA appear to be highly subjective, and often manipulative, in the Interpretation phase. It is common practice in LCA to postpone the choice of the indicator to the end of the study: only a few, out of the more than 20 midpoints in the output, are selected then that support the desired outcome (for companies this is a cleaver way of greenwashing, for NGOs it is a cleaver way of spinning in their PR). Hence the requirement in the ISO for “both justified and consistent” indicators, that have to be selected in the goal and scope stage.

In LCA studies on innovation of materials, products, and services, endpoints and single indicators are advised (either eco-costs, ReCiPe, or Ecological Footprint), to avoid the aforementioned manipulation of conclusions. These endpoints and single score systems are solutions for an “integral” environmental approach. These systems are less accurate, however, are well defined and transparent, which is much more acceptable than the subjective selection of a LCA practitioner. Although the objections of ISO 14044 in Section 4.4.3.4 and 4.4.5 are clear (“Weighting …. shall not be used in LCA studies intended to be used in comparative assertions …“, the majority of the modern scientist abandoned the idea that weighting is forbidden in LCA: it cannot be avoided in damage based systems (See Kägi et al. Session “Midpoint, endpoint or single score for decision-making?”—SETAC Europe 25th Annual Meeting, May 5th, 2015. Int J Life Cycle Assess (2016) 21:129–132)

Eco-costs, however, does not have the issue of weighting, since the issue of “different individuals, organizations, and societies may have different preferences“(section 4.4.3.4) does not play a direct role in the calculation system.

Note that single score systems have each their own assumptions in modelling (as midpoint systems have). Therefore all these systems have their inherent value choices, and areas of application.

Summarizing pro’s and con’s of eco-costs

eco-costs are:

– less accurate than midpoints (the calculation pathway is longer)

– more accurate than damage based endpoints, i.e. the 3 endpoints for the 3 Areas of Protection (since the calculation pathways of these endpoints are much longer and need a lot of extra assumptions)

– more accurate than damage based single indicators, i.e. the sum of the weighted endpoints that requires the choices of groups of people

– less suitable for ‘awareness building’, since that can better be based on damage

– more suitable for business people, since they “understand money” and are interested in the costs of prevention

– more suitable for governments that must design implementation strategies for the coming 30 years, since such strategies are restricted by the available budget in society

– more suitable to C2C calculations (together wit ReCiPe and Ecological Footprint), since they combine material scarcity indicators (the issue of materials depletion) and carbon footprint (the issue of the preference of the biosphere).

– suitable for people who are convinced that the required targets can be reached by innovation in combination with governmental regulations (i.e. by building a cleaver, new, economy)

– not suitable for groups of people that are convinced that it is fundamentally not possible to reach the required targets with innovation in a society that is based on money.