General remarks

(1) The project approach is: (step 1) collect data (step 2) make calculation with the tool (step 3) decide on what is ‘material’ and what is ‘not-material’ (in kg CO2 and in eco-costs, where high eco-costs are related to high financial risks), and decide on your mitigation strategy: what is first and what is next? (step 4) make you calculation for the next 5 years (example: the excel tool, sheet ‘calculation results 2029’) (step 5) write your mitigation plan with expected results, see sheet ‘overview results’ (step 6) do the compliance check

It is common sense that you take the ‘low hanging fruit’ first (e.g. start with a procurement strategy that includes CO2 emissions). A cleaver investment strategy is is bit more complex: see section 9.3 “timing of improvement projects” of the book “Eco-efficient Value creation“.

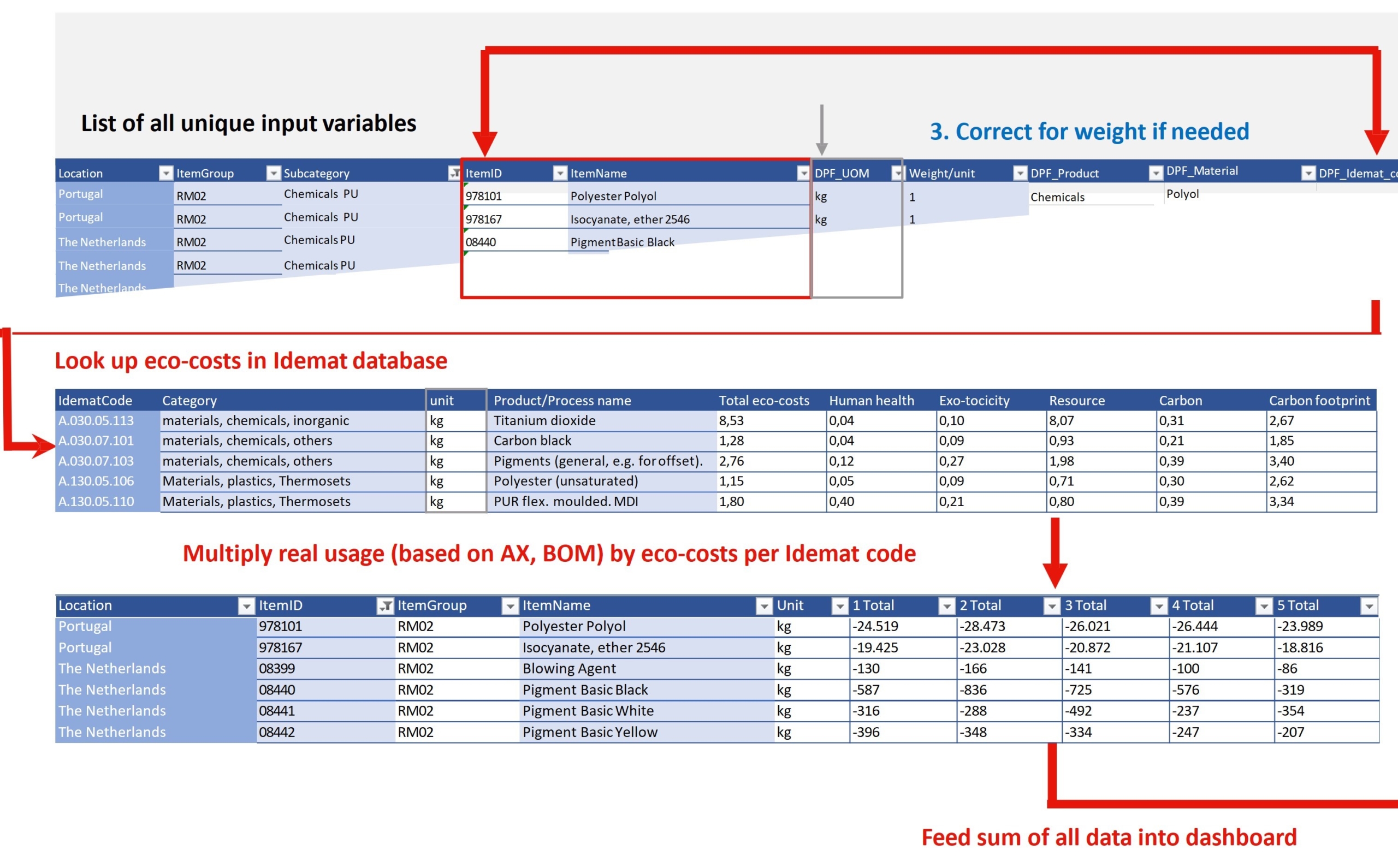

(2) Where possible, apply data which are readily available from your accounting (or ERP) system, and convert these data from euros to kilograms, liters, or kilometers by factors that are applicable to that year. The Idemat data in the tool are in IS units: m for length , s for time, kg for weight, MJ for electricity (in stead of kWh). So it is likely that you have to apply an extra conversion step.

Often you don’t know the kilograms for car fuels; apply than the norms for lease cars, lines A.070.03.101 trough A.070.03.401 of the Idemat file.

(3) There are a lot of details in the formal documents of the EU (the authors tried to add everything that they could think of). Depart, however, from your common sense, since (a) a lot of tables and lists are provided with the instruction ‘may’, rather than ‘shall’ (b) the basic assumption of your work is that pollution must be ‘material’ so things that are negligible can be left out. So what you report is your own decision, as long as you can prove that what you left out is ‘not-material’. So your calculation list must include ‘everything’ (material and not-material) what seems to be relevant to you and your accountant: you only know what is ‘not-material’ after your calculation.

(4) In ‘CSRD Essentials‘, page 33, “The importance of including value chain Impacts, Risks and Opportunities”, it is described that databases like Idemat must be used to get the multipliers that are needed for the calculations. On the long term, it is expected that every supplier can provide the required data of his products. However, the amount of calculations that are needed are that high, that it is expected that more than a decennium is needed to fill this data gap.

(5) The compliance check can be finalized at the end (don’t start your project with a compliance check), since the compliance is highly related to your double-materiality choices: this helps reduce the 1,400 data points to what is relevant for your company. Note further that: (a) many of these data points are not “shall disclose” but are “may disclose” (b) are not required the first year

(6) In LCA, so called ‘double counting’ is to be avoided. In CSRD, however, double counting is not an issue: it seems to be everywhere. It is embedded in the combination of E2, E3, and E4, as well as in the Scope 3 reporting on the value chain, upstream and downstream.